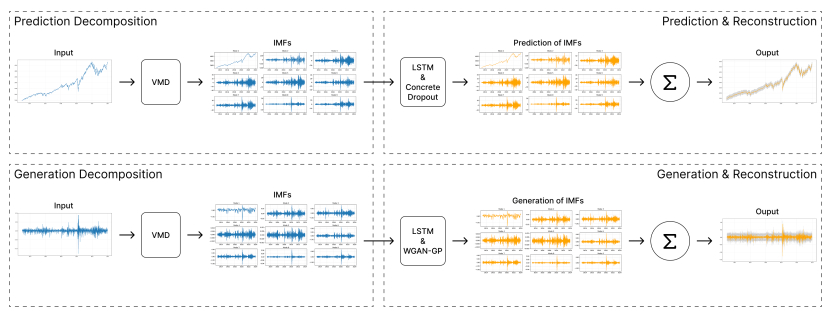

Figure 1. Overview of the dual-path uncertainty modeling framework

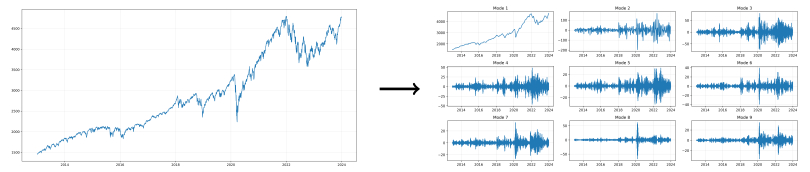

Figure 2. Raw price of Standard & Poor's 500 (S&P 500) index (left) and its intrinsic mode functions (right)

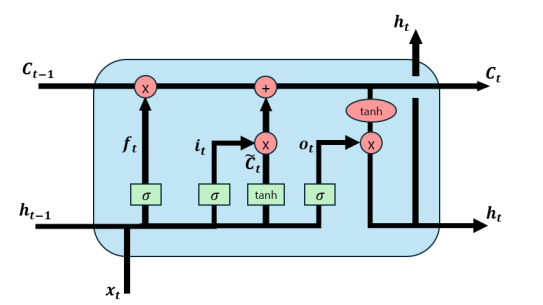

Figure 3. LSTM cell structure

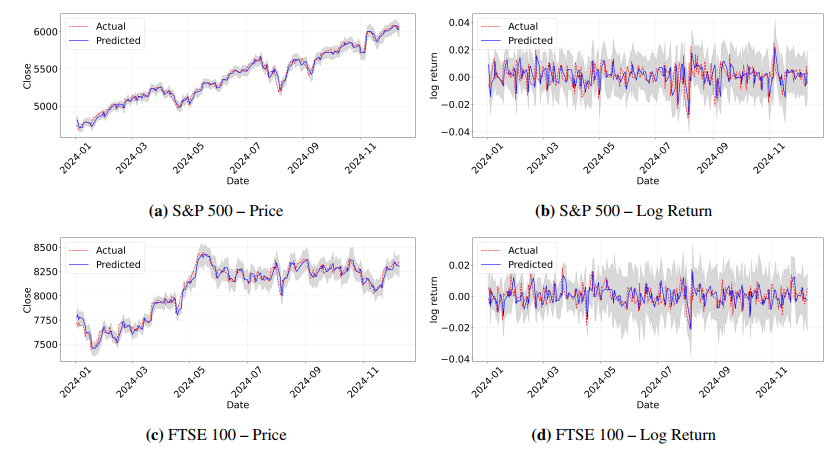

Figure 4. One-step-ahead forecasts with daily 95% posterior predictive intervals via Monte Carlo-dropout (gray shaded region) for the S&P 500 and FTSE 100 using the VMD–LSTM–CD model

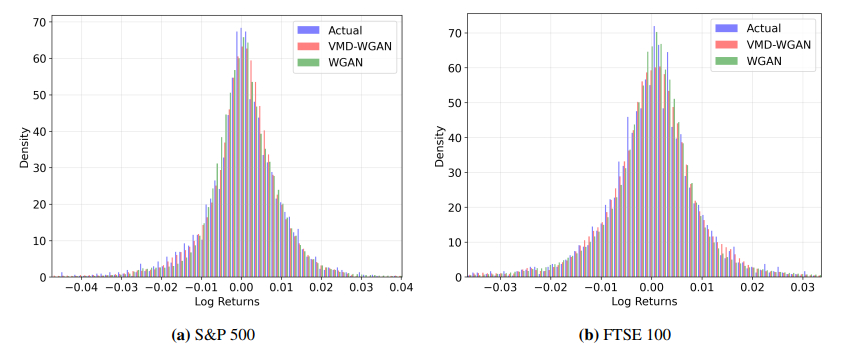

Figure 5. Unconditional histograms of daily log-returns for the actual series (blue) and synthetic samples generated by VMD–WGAN (red) and WGAN (green) over the in-sample period 2013–2023

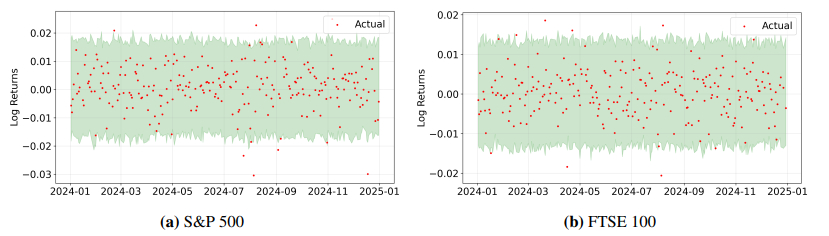

Figure 6. Empirical 95% generation bands (green) and actual values (red) from the VMD–WGAN model. The green shaded area represents the empirical 95% generation band, computed from multiple samples generated by the proposed model. These bands capture the distributional uncertainty learned from the training data, rather than classical statistical confidence intervals

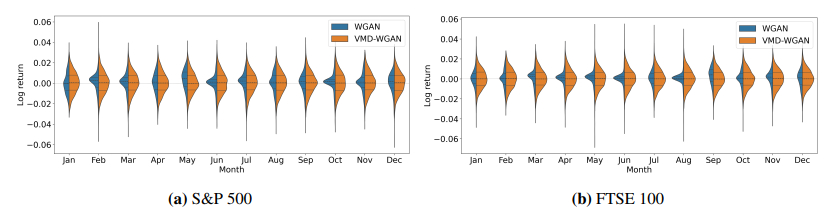

Figure 7. Monthly distributions of generated log-returns from WGAN and VMD–WGAN models for S&P 500 and FTSE 100

DownLoad:

DownLoad: